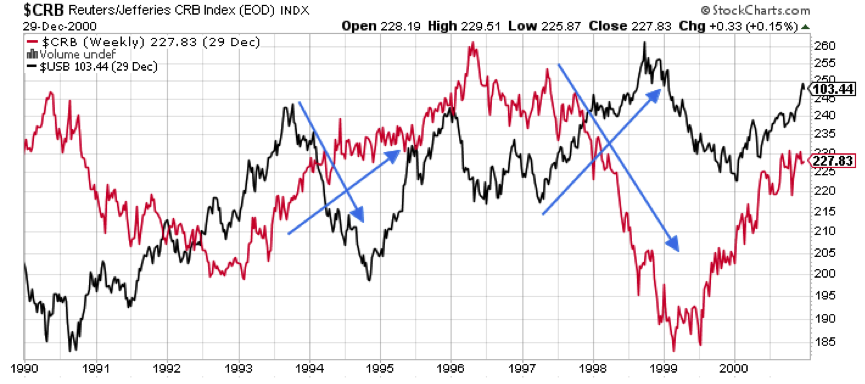

The 2000s: why some exceptions occurred to the inverse relationship?

During the first two decades of this century, commodities and bonds continued to be inversely correlated but with two major exceptions: 2002/2003 and 2007/2008. In 2002, both markets trended upward even though roughly a year later, bond prices started to fall while the CRB index continued to appreciate (resuming their inverse relationship). What happened during 2002/2003? In the midst of fears of deflation (deflationary CPI and PPI figures), the stock market crashed. The Fed, worried with the aftermath of the crash, eased monetary policy, pushing interest rates lower (and bond prices higher), to stem the drop in the stock market. Hence, the dollar (by that time, a low-yielding currency) fell sharply which caused commodity prices to turn up before stocks, which was unusual. Some observers pointed out that the U.S. Government abandoned its strong dollar policy in order to boost prices. In addition, another reason explained why bond prices also rose during the second half of 2002 and it is related to which commodities did the rallying and the interpretation made by bondholders. In the third quarter of the same year, and as a result of a drought in the U.S. Midwest, corn and other grain prices soared which gave a big boost to the CRB index. Grain markets react to weather. However, copper prices, which are more closely correlated to the state of the economy and is deemed to be a better economic indicator than grain markets, fell dramatically over the same period. It appeared that bond traders were more concerned with the weak economic message sent by a falling copper than by the temporary rally occurred in the grain markets. And as copper was negatively correlated to bond prices, bondholders decided to keep their positions despite rising CRB index.

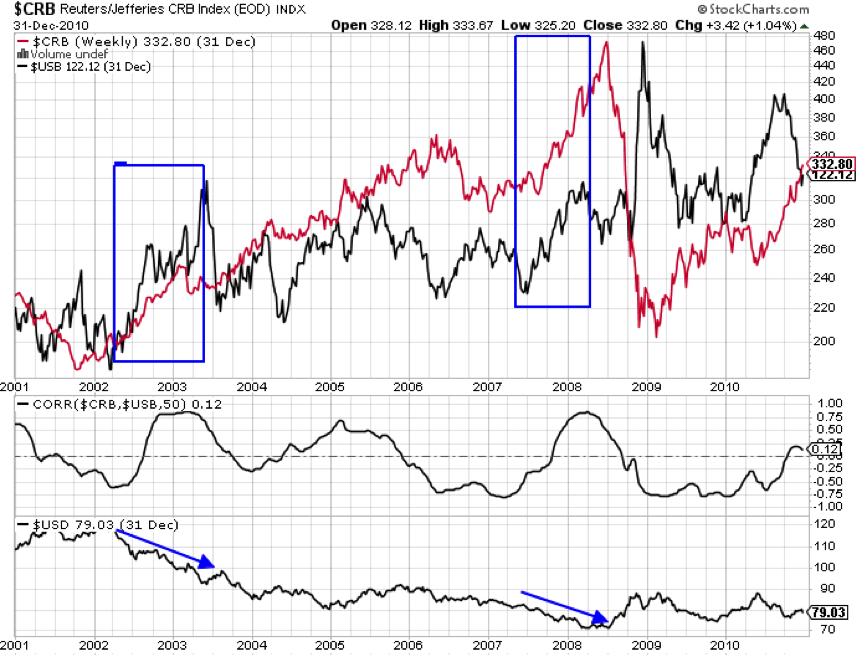

In 2006, falling commodity prices helped bond prices to bounce back. One year later, another exception took place, more precisely during the second half of 2007 and the first semester of 2008, periods when both markets trended higher. This was caused by negative trends in the stock and dollar markets. The former started to fall dramatically during the second half of 2007, which caused a massive flow out of stocks and into Treasury bonds. Additionally, the Fed, worried with the aftermath of the crash, eased monetary policy, pushed interest rates lower (and bond prices higher), to attenuate the drop in the stock market (resulting from the bursting of the housing bubble). Hence, the dollar continued to fell sharply which pushed commodity prices higher. This change to the normal bond/commodity relationship was kept until the start of the second semester of 2008, when commodity prices started to weaken due a US Dollar bottom (and bond prices to strengthen).

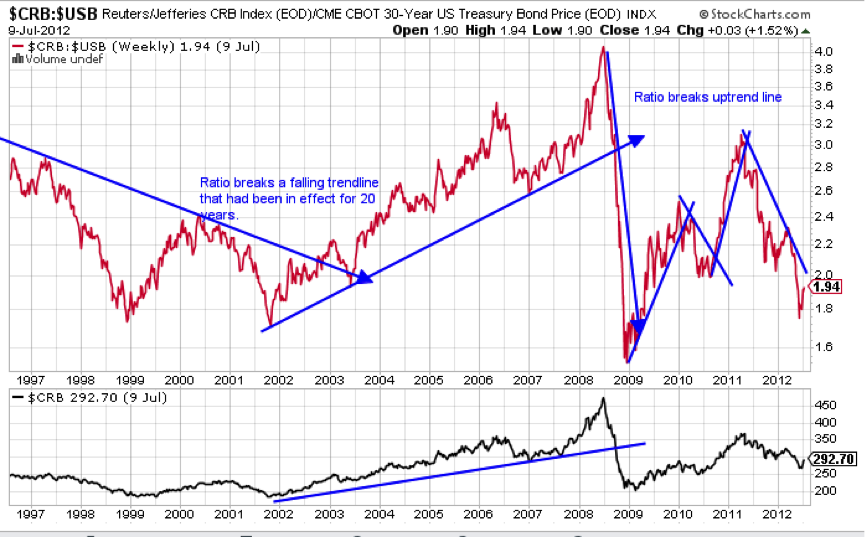

The CRB Index/30-year Treasury Bond Ratio: historical behaviour

Ratio charts are useful indicators to determine which asset class is stronger at any point in time and to spot trends changes. Traditional technical analysis indicators such as moving averages, support, resistance levels and so forth can also be applied to these charts. The commodity/bond ratio peaked in 1981 and fell for about 20 years meaning that bonds were a better place to be compared to commodities. However, and from 1986 to mid-1988, commodities outperformed bonds by about 30%. During part of the same period (mid-1987 until mid-1988), commodities also outperformed stocks by 25%. This period was characterized by a stock market crash and an upward movement in commodities due to the Midwest drought.

The following chart plots the ratio from 1996 until 2012. In 2004, a downward trend line that was in place since 1984 was broken and a rising ratio began (favoring commodities over bonds) until 2008, year in which Treasuries soared and commodities plunged (during the height of the financial crisis). I have drawn some trend lines in the chart in order to make it easier to identify turns. A rising ratio indicates that the commodity market is the place to be whereas a falling ratio indicates the opposite.

Like!! Really appreciate you sharing this blog post.Really thank you! Keep writing.

Hey there! I just want to offer you a huge thumbs up for your excellent info you have

here on this post. I am coming back to your blog for more soon.