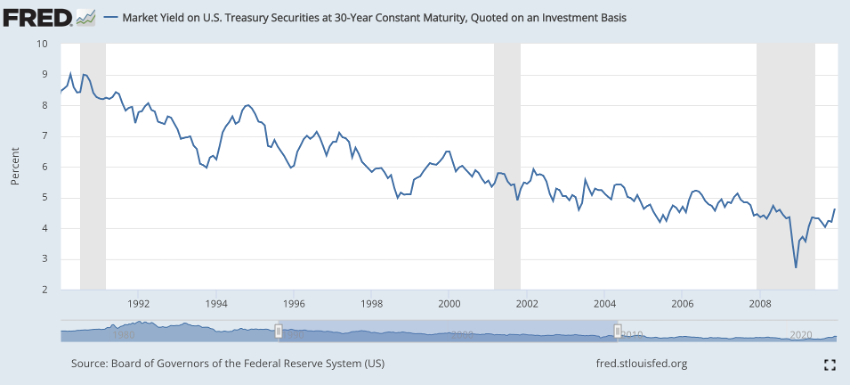

During the second half of 2007 and the first semester of 2008, both bonds and commodities rallied together (black and red up arrows). In the chaos of this stock market crash, the inverse correlation between commodities and bonds was temporarily lost!

As was the case during part of the dot-com market crash, this exception was caused by the decreasing stock and dollar prices. The stock market started to fall dramatically from October 2007 onwards. This caused a massive flow out of stocks and into treasury bonds (upper black line).

By this time, the Fed, worried about the slumping housing sector, tightening credit market and stock market volatility, eased the monetary policy and pushed interest rates lower. And you all can guess what this led to: higher bond prices. And as the U.S. dollar was plunging continuously (green down arrow), the commodity rally kept going (red up arrow).

As a result, bond and commodity prices rose together roughly until the beginning of the second semester of 2008 when the commodity prices started to weaken mostly due to a US Dollar bottom. Furthermore, with short-term interest rates near zero, poor economic growth and a real threat of deflation, the Fed began, in November 2008, the first round of an unconventional approach to monetary policy known as quantitative easing. Bonds kept rising as an appeal of safety and income. And the commodity correction also helped push bond prices sharply higher.

So, for the last six months of 2008 and until the stock market bottom in March 2009, commodities and bond prices reverted to their normal inverse correlation.

Major Takeaways:

– The threat of a deflationary environment dampened the normal bond-stock relationship. That said, unlike of what happened in the 1970s and 1980s, falling bond yields (or rising bond prices) preceded the 2008 stock market crash. So, falling bond yields became bad for stocks.

– As you can see in the chart, plunging interest rates and bond yields during the 1990s and 2000s are usually symptomatic of both disinflationary and deflationary environment.